Why Dollar Strength Matters for Property Investors Watching Rates

A firmer US Dollar is not just a currency story. For real estate investors, it is a signal about capital costs, lending conditions, foreign buyer behavior, and the timing of refinancing decisions.

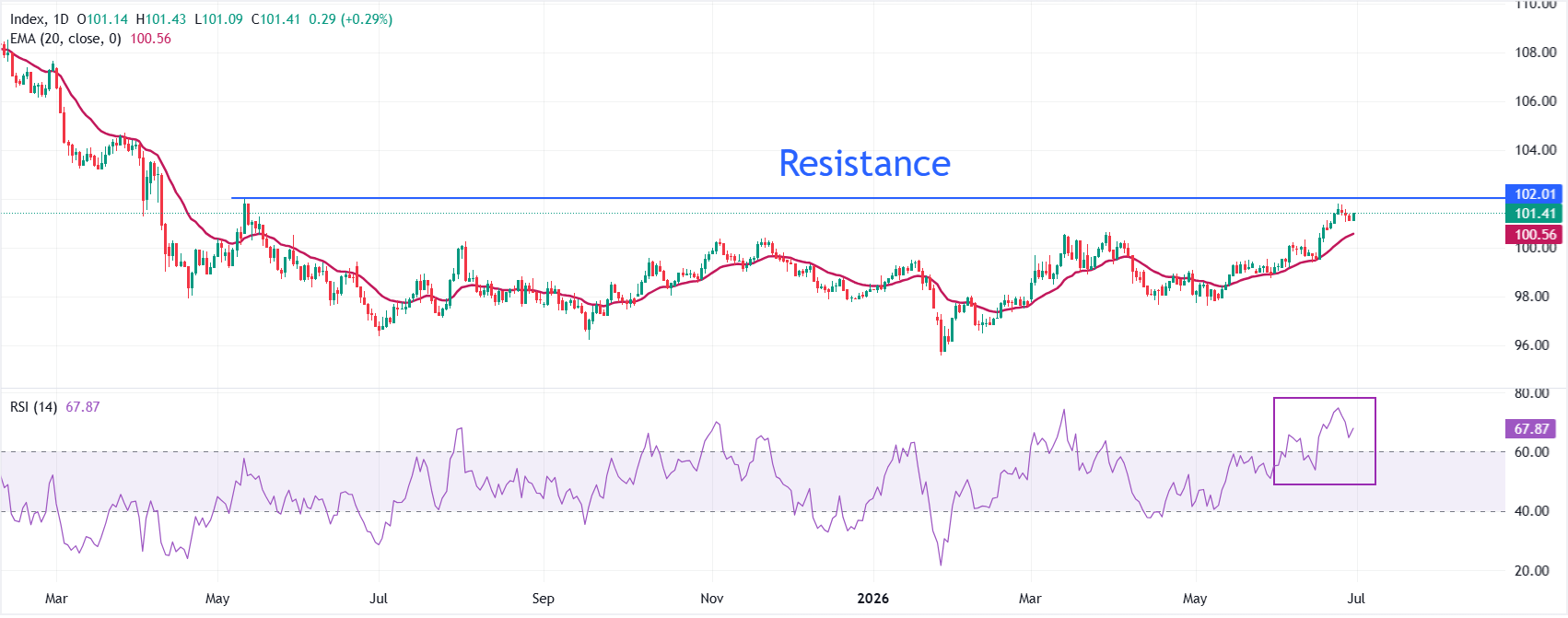

According to FXStreet, the US Dollar Index rebounded after a three-day decline, rising 0.3% to trade near 101.40 as investors turned cautious ahead of the June US Nonfarm Payrolls report. The employment data is expected to show 110,000 new jobs, down from 172,000 in May, with unemployment holding at 4.3%.

That matters because property markets remain highly sensitive to the direction of Federal Reserve policy. Stronger employment data would give the Fed more room to keep policy restrictive. Softer data would strengthen the argument for eventual easing. Either outcome feeds directly into mortgage rates, commercial debt pricing, cap rates, and buyer confidence.

For residential investors, the key issue is affordability. A stronger Dollar often reflects expectations of tighter monetary conditions or safe-haven demand. If bond yields follow, mortgage rates may remain elevated for longer. That keeps monthly payments high, limits first-time buyer activity, and can support rental demand in markets where would-be owners stay in the rental pool.

For landlords, this is a mixed signal. Higher financing costs make acquisitions harder to underwrite, particularly for leveraged buyers. But constrained homeownership can strengthen occupancy and rental resilience in supply-limited cities. The opportunity is not in chasing yield blindly. It is in identifying submarkets where wage growth, household formation, and limited new stock support rent durability.

Currency movement becomes a property signal when it changes the cost of capital.

Commercial real estate investors should read the Dollar move through the refinancing lens. If the Fed remains cautious, debt maturities become more difficult to manage, especially for assets bought at lower cap rates during cheap-money years. Office, secondary retail, and overleveraged multifamily remain exposed where income growth cannot offset higher interest expense.

There is also an international angle. A stronger Dollar makes US property more expensive for foreign buyers converting from weaker currencies. That can cool demand in luxury residential and gateway markets. At the same time, global capital often still views US real estate as a defensive store of value during uncertainty. The distinction is important: discretionary buyers may pause, but institutional capital can remain active if pricing adjusts.

FXStreet noted that the Dollar Index remains above its 20-period exponential moving average around 100.56, with resistance near 102.00 and a possible move toward 103.00 if momentum continues. For property investors, those levels are less important than the message behind them: markets are still positioning around inflation, employment, and central bank patience.

The practical takeaway is simple. Investors should stress-test acquisitions against higher-for-longer borrowing costs, avoid relying on near-term rate relief, and prioritize assets where income is defensible. In this environment, balance-sheet discipline is not conservative. It is competitive advantage.

Source: FXStreet

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")