Toronto’s Condo Reset Is Becoming an Investor Signal

Toronto’s condo market is beginning to look less like a distressed asset class and more like a repriced entry point. For buyers who were priced out during the pandemic boom, the numbers now point to a familiar benchmark: 2019 affordability.

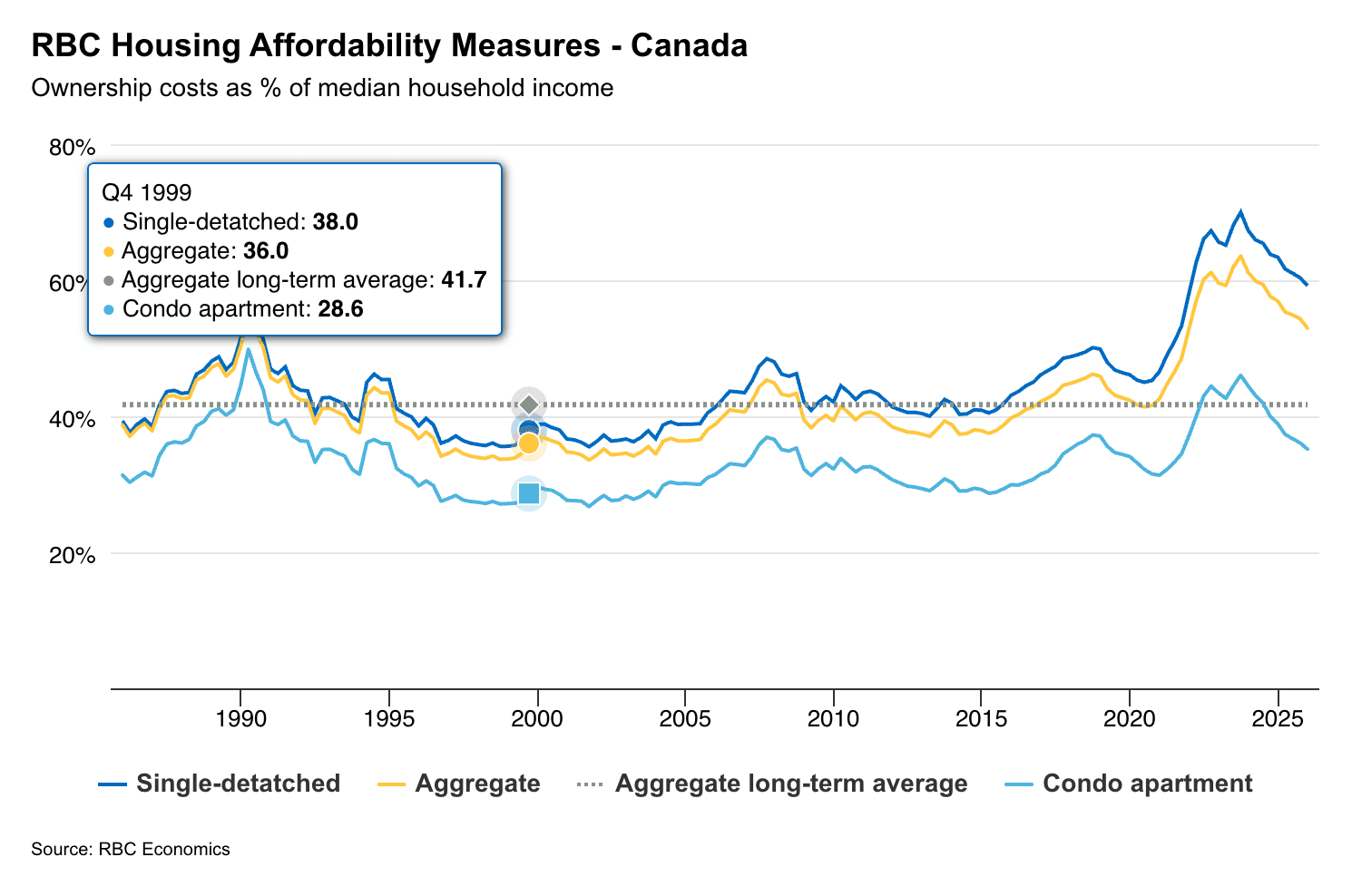

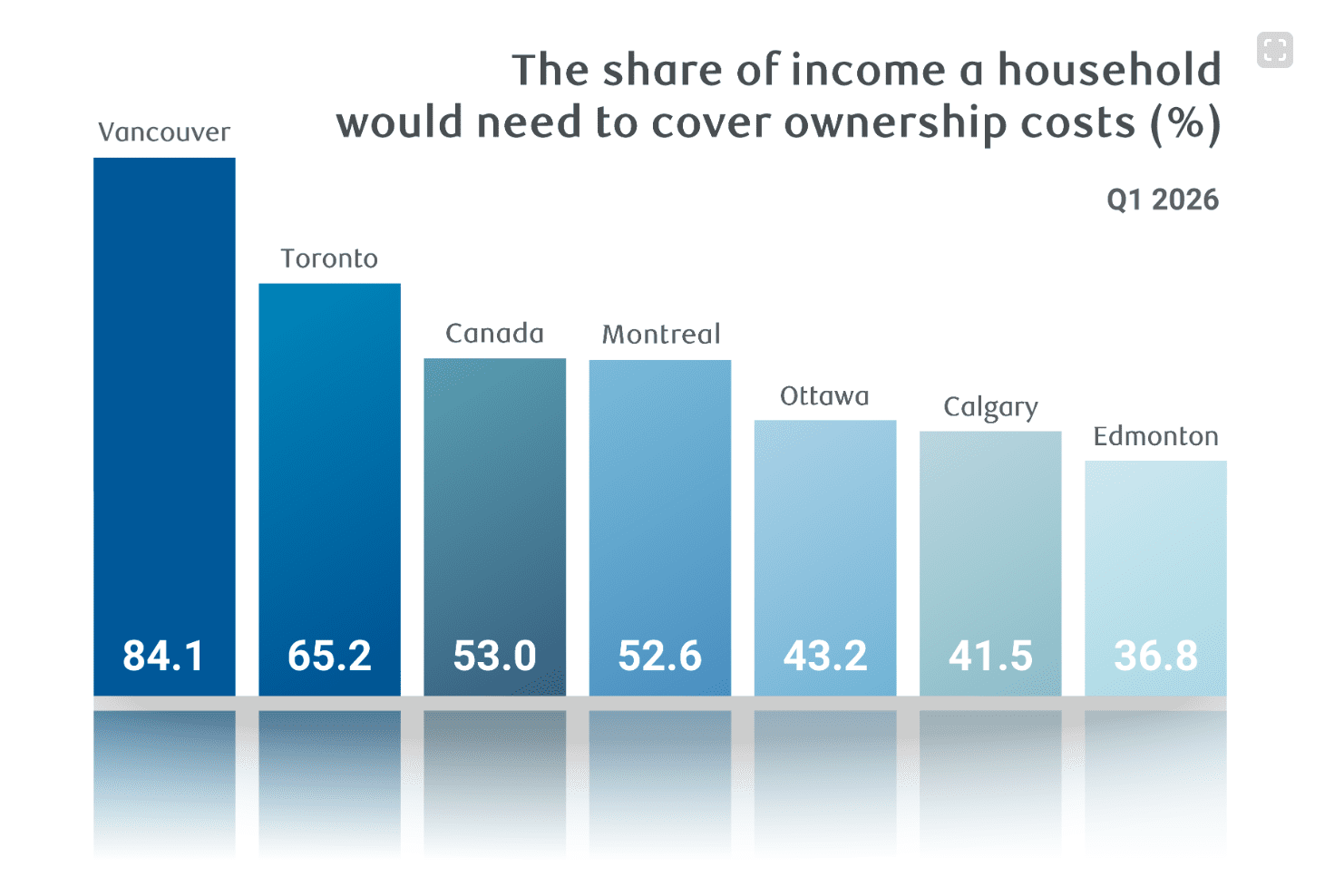

According to a new Royal Bank of Canada report covered by Real Estate Magazine, falling condominium prices in the Greater Toronto Area have brought ownership costs for condos back to roughly pre-pandemic levels. RBC’s affordability measure for Toronto condos declined to 35.2 per cent in the first quarter of 2026, meaning a representative household would need about that share of pre-tax income to cover ownership costs.

For investors, the significance is not simply that condos are cheaper. It is that affordability has improved while the detached market remains structurally inaccessible for many households. RBC noted that ownership costs for a typical detached home in Toronto still consume more than 80 per cent of representative household income. That gap matters. When ground-oriented housing is out of reach, demand often redirects toward smaller ownership formats and rental housing.

This is where the condo correction becomes investable. A market that has already absorbed several years of price weakness can offer better downside protection than one still trading near peak affordability stress. Toronto condos are not universally cheap, and carrying costs remain sensitive to interest rates, maintenance fees and rent levels. But relative to the detached segment, the value spread has widened.

The opportunity is not in assuming Toronto condos will rebound quickly. It is in recognizing when a major urban asset class has moved from overpriced to negotiable.

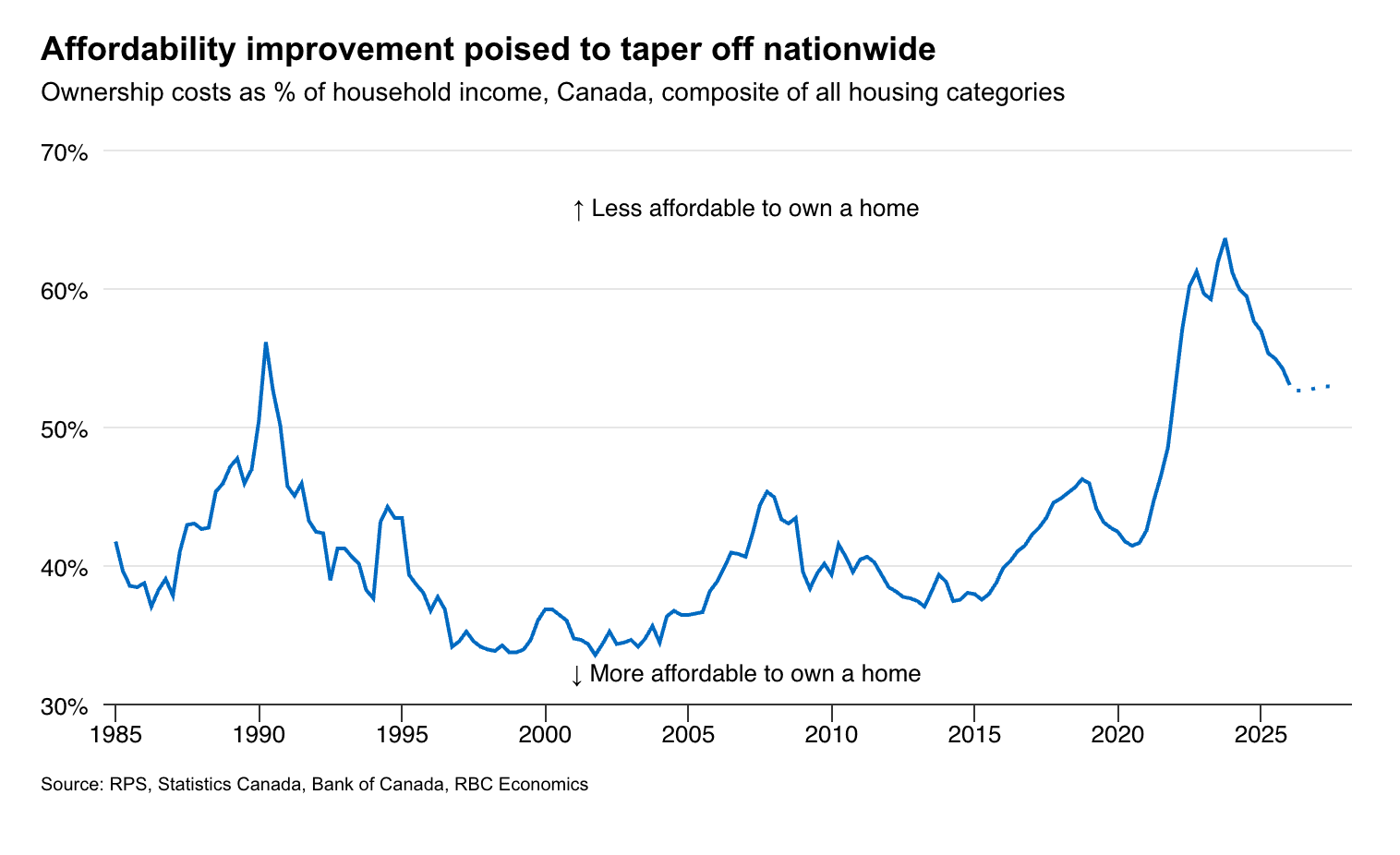

Nationally, RBC’s housing affordability measure improved to 53 per cent in the first quarter, its best reading in four years. That improvement was led mainly by Toronto and Vancouver, where prices have softened. Yet both cities remain Canada’s least affordable major markets overall, which should keep investor expectations disciplined. Better affordability does not mean broad affordability.

The more interesting comparison is with smaller markets. RBC found that affordability has continued to deteriorate in places such as Montreal, Quebec City, Winnipeg and St. John’s. Montreal’s condo affordability measure has now moved above Toronto’s for the first time in 16 years, while Halifax has narrowed the gap to less than three percentage points behind Toronto.

That reversal carries a clear allocation message. Smaller markets that once looked like affordable alternatives have become more expensive on an income-adjusted basis, while Toronto’s condo segment has corrected. Investors chasing lower headline prices outside the GTA may now be paying more for weaker liquidity, thinner rental depth or less diversified employment bases.

The risk is timing. RBC expects further affordability gains to slow as price declines taper and interest rates appear to have passed their cyclical lows. If mortgage costs stop falling, future affordability improvement will depend more on income growth than asset price weakness. That means buyers waiting for another large discount may find the window narrows before it becomes obvious.

For KG Invest readers, the practical takeaway is to underwrite Toronto condos with precision. Focus on buildings with strong reserve funds, transit access, efficient layouts and rental demand that survives slower resale periods. The broad market may be stabilizing, but returns will still be made unit by unit, not by relying on a citywide rebound.

Source: Real Estate Magazine

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")