Toronto’s Application Slowdown Is Becoming a Pipeline Risk

Toronto’s development market is no longer just absorbing a difficult financing cycle. It is now showing a measurable contraction in future housing supply. UrbanToronto’s latest UTPro data shows that new development applications in the city fell sharply again in the second quarter of 2026, deepening the slowdown that began earlier in the year and raising a more strategic question for planners, developers, lenders, and governments: what happens to housing delivery three to five years from now when today’s intake pipeline is this thin?

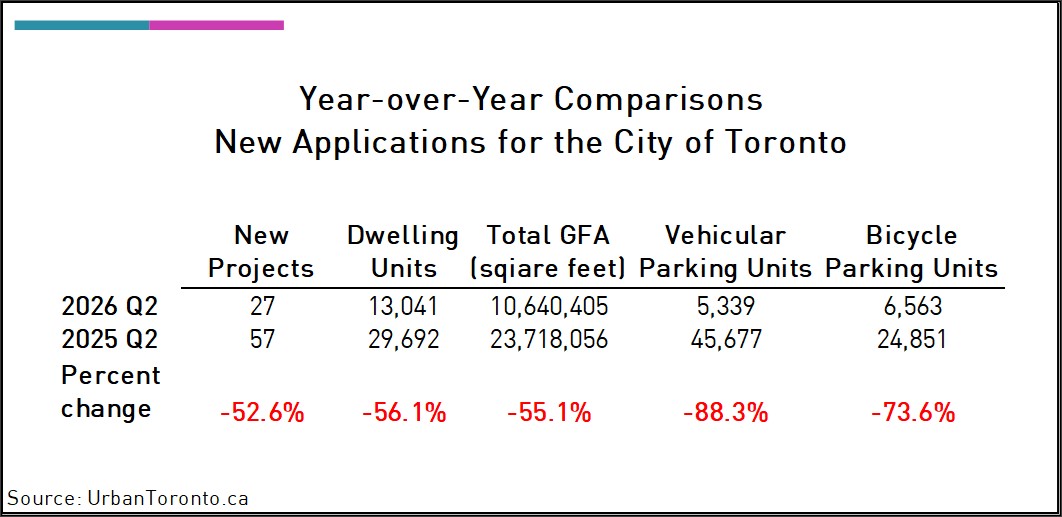

The headline numbers are material. According to UrbanToronto, Q2 2026 produced 27 new development applications, down from 57 in the same quarter last year. Proposed residential units dropped to 13,041 from 29,692, a decline of 56.1 percent. Total gross floor area fell by 55.1 percent. These are not marginal movements. They represent a broad pullback in the volume of projects entering the municipal review system.

For the development industry, the issue is not only that fewer applications are being filed. It is that the projects being held back today are the potential construction starts, occupancy dates, tax base additions, and infrastructure load forecasts of the early 2030s. Toronto’s approvals system already operates with long lead times. When fewer projects enter the front end, the downstream effect is delayed but significant.

The composition of the remaining pipeline also matters. Q2 applications included seven condo projects and 14 rental projects, suggesting that purpose-built rental remains active relative to ownership housing. That is consistent with current market reality. Condo presales remain challenged by affordability, investor fatigue, elevated carrying costs, and construction pricing. Rental, while also under pressure, benefits from deep structural demand and a stronger policy narrative. Still, rental feasibility is not automatic. Land cost, development charges, interest rates, operating assumptions, and property tax treatment continue to determine whether a rental site can actually proceed.

The parking numbers are one of the strongest urban signals in the report. Vehicular parking spaces fell 88.3 percent year over year, from 45,677 to 5,339. That reflects more than a smaller application pool. It points to a different development geography and a different pro forma logic. Projects near transit, in nodes, and in corridors can reduce parking ratios and improve land efficiency. In a high-cost construction environment, every avoided underground parking stall can improve feasibility. The decline also aligns with Toronto’s broader planning direction, where transit-oriented density is increasingly the only practical path to adding scale.

A slowdown in applications is not a pause in growth pressure. It is a warning that the city may be underfeeding its future housing pipeline.

There is also a density story beneath the decline. UrbanToronto notes that unlike Q1, Q2 included a taller and denser mix of proposals, with an average proposed building height of 81.9 metres and one application reaching 250.5 metres. The most intense projects are still being advanced, likely on sites where transit access, planning policy, land assembly, and scale can support the economics. This suggests the market is becoming more selective. Marginal sites are being deferred. Strong sites are still moving, but they must carry more density to justify risk.

For municipalities, this is a policy stress test. If Toronto wants housing supply to recover, it cannot rely only on demand returning. It needs predictable approvals, infrastructure capacity, development charge certainty, and zoning permissions that make mid-rise, high-rise, and rental projects financeable. For developers and investors, the lesson is equally clear: the next cycle will favour sites with transit proximity, as-of-right or near-as-of-right density, limited parking burden, and a credible path through approvals.

The market is not dead. It is filtering. The question is whether Toronto’s planning and infrastructure systems can help viable projects move before today’s application slowdown becomes tomorrow’s supply shortage.

Source: UrbanToronto

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")