The GTHA Crane Count Is Holding, But the Growth Map Is Starting to Shift

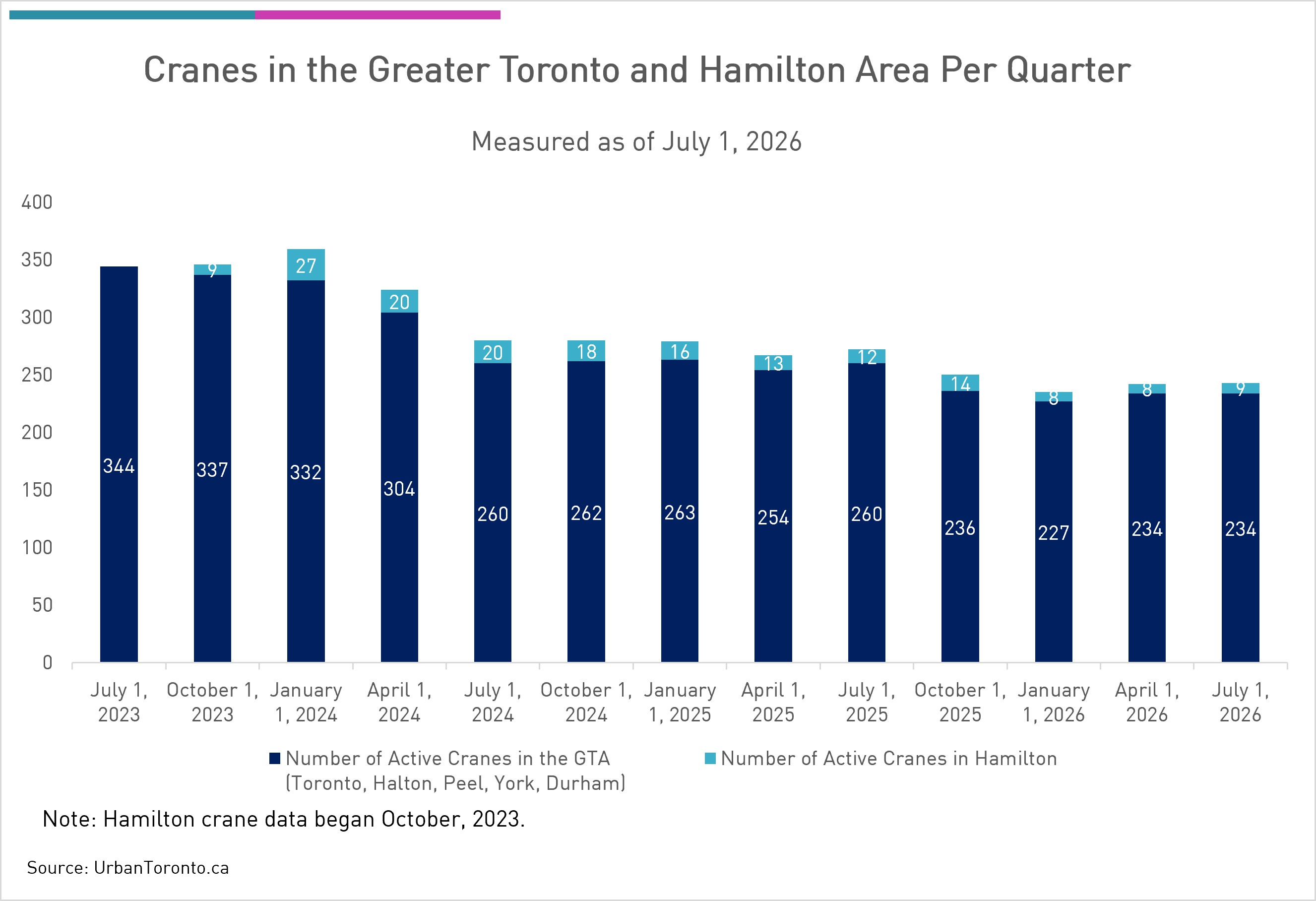

The Greater Toronto and Hamilton Area still has a skyline full of construction activity, but the strategic signal is not simply the number of cranes. It is where they are holding, where they are falling, and where momentum is quietly moving. UrbanToronto reports that 243 cranes were active across the GTHA as of July 1, 2026, down seven from the same period last year but up one from the previous quarter. For developers and planners, that is not a collapse. It is a market recalibration.

Crane counts are an imperfect but useful proxy for development confidence. They show what has already cleared zoning, financing, sales, approvals, procurement, and construction mobilization. In a region where housing demand remains structurally high, a steady crane count suggests the pipeline has not stopped. But it also shows that new supply is being delivered through a narrower feasibility window, with construction costs, interest rates, development charges, and absorption risk still shaping which projects advance.

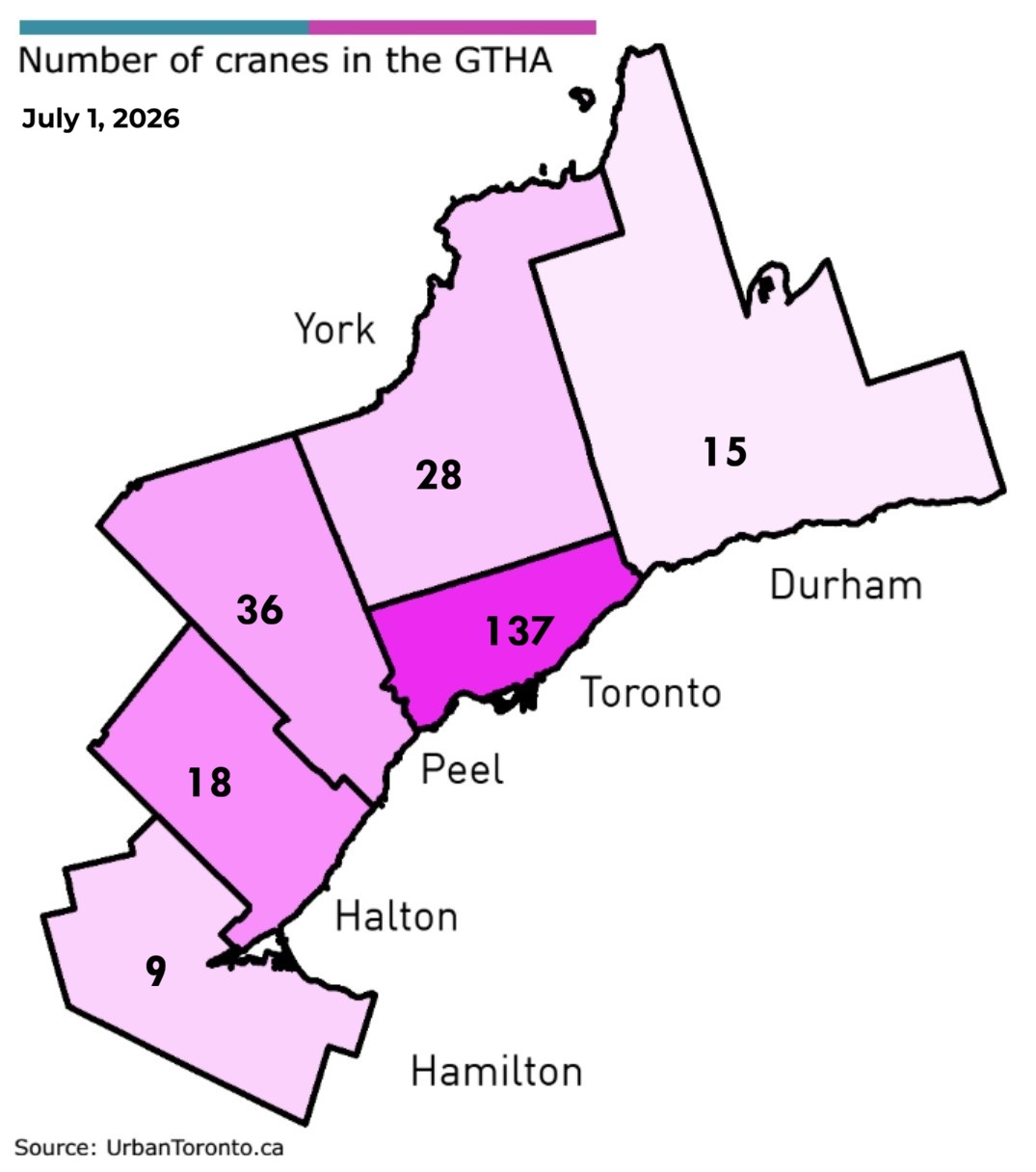

The regional movement matters. According to UrbanToronto’s UTPro data, Toronto, Hamilton, Halton, and York saw year-over-year crane declines, while Durham and Peel recorded slight increases for the second consecutive quarter. That pattern speaks to more than construction timing. It reflects how growth pressure is distributing across the urban region, especially as buyers, renters, and builders respond to land pricing, transit access, municipal approvals, servicing capacity, and relative affordability.

Toronto remains the dominant development market, but its constraints are increasingly visible. High land values, complex approvals, tall-building construction costs, and policy uncertainty make many projects harder to underwrite. The projects that proceed tend to be deeper into the planning process, better capitalized, or located in areas with stronger transit, rental demand, or intensification logic. A modest decline in Toronto cranes does not mean demand has weakened. It means execution has become more selective.

Peel and Durham gaining cranes is worth watching. These markets sit at the intersection of population growth, regional rail investment, highway access, employment lands, and lower relative acquisition costs. They are also places where municipalities are under pressure to accommodate density without relying only on traditional low-rise expansion. If infrastructure and approvals align, these regions can absorb a larger share of the GTHA’s next wave of housing construction.

A steady crane count in a high-demand region is not stability in the old sense. It is a sign that only the most feasible projects are making it through the filter.

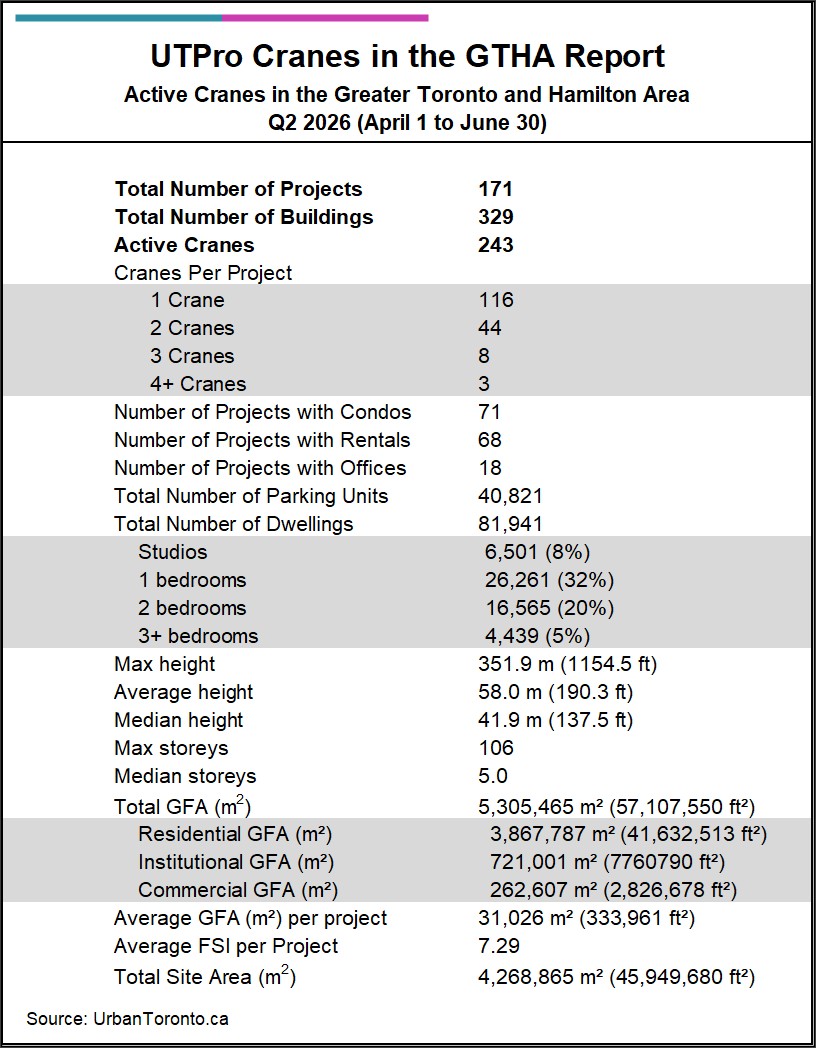

The headline figure is still substantial. UrbanToronto identifies 171 projects using 243 cranes to build 329 buildings, contributing 81,941 dwelling units across the GTHA. The typical crane-supported project height is 41.9 metres. That points to a market where mid-rise and high-rise delivery remain central to the region’s housing supply, particularly in nodes, corridors, and areas where municipal policy is pushing intensification over outward expansion.

The next question is whether the recent improvement in new construction starts can translate into a broader crane recovery. If starts continue to rise, crane counts should eventually reflect that. But the lag is important. Approvals, financing, shoring, excavation, and procurement all take time. Investors should not read one quarter as a cycle turn. They should watch consecutive starts, pre-construction absorption, rental underwriting, municipal fee changes, and whether governments move from housing targets to actual servicing and approval capacity.

For large landholders, the message is clear: the GTHA is still building, but growth is becoming more tactical. Land near transit, infrastructure, and municipalities with approval discipline will carry a premium. Sites that depend on optimistic density, slow servicing, or fragile pro formas will remain exposed. The cranes are still in the sky. The opportunity is in understanding which municipalities are preparing the ground for the next ones.

Source: UrbanToronto

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")