The Week Property Investors Should Watch the Labour Market

Real estate investors do not need every macro data point. They need the ones that move borrowing costs, tenant demand, construction budgets, and exit values. This week’s calendar matters because it sits directly at that intersection.

Yardeni QuickTakes framed the coming week around June employment, manufacturing surveys, consumer confidence, and Eurozone inflation. For property investors, the central question is simpler: does the economy remain strong enough to support rents, but not so hot that interest rates stay higher for longer?

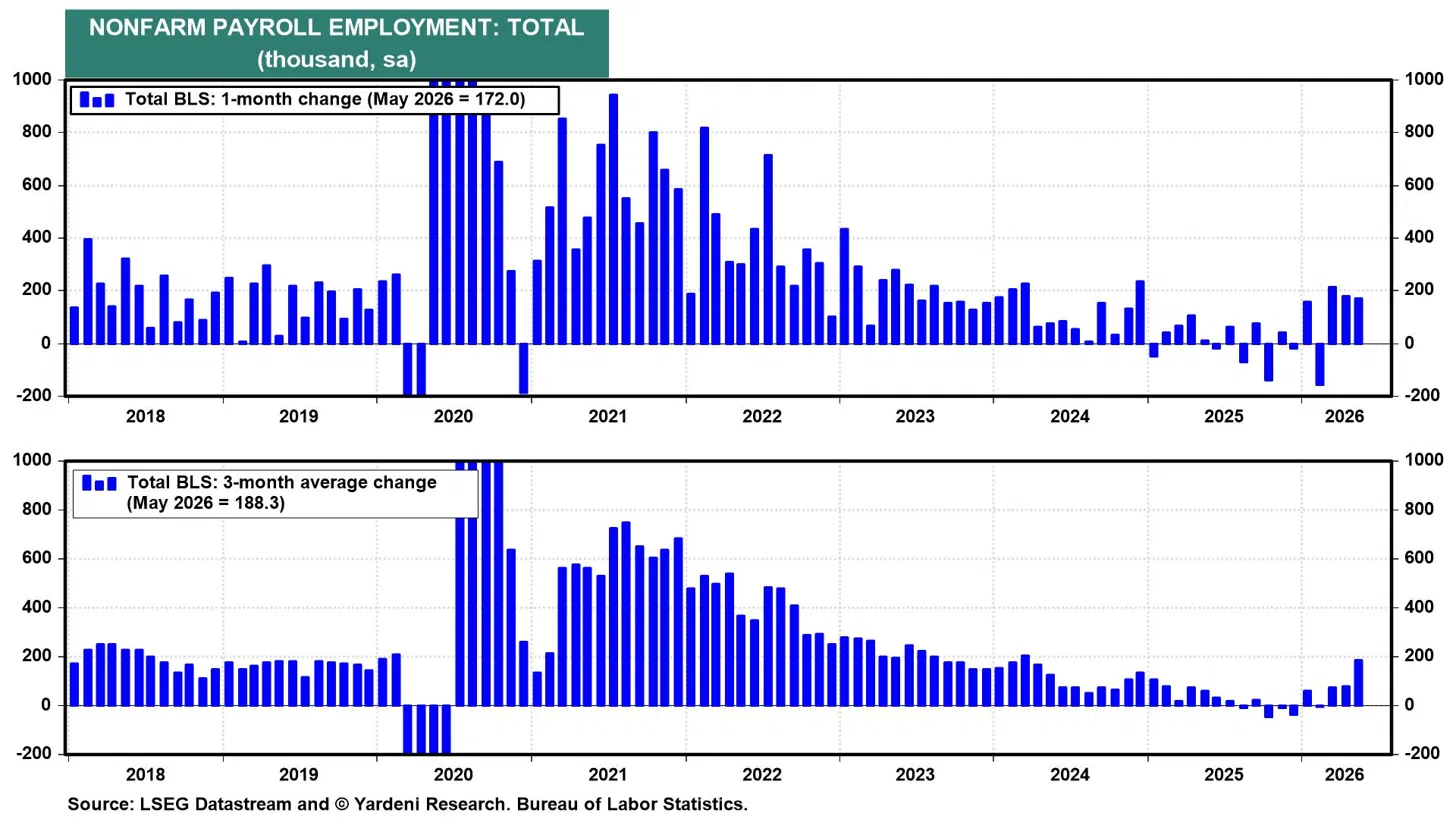

The June employment report is the key release. May payrolls rose by 172,000, with the three-month average at 188,300 after revisions added 93,000 jobs to March and April. That is not recessionary data. It signals an economy still capable of supporting household formation, leasing activity, and consumer spending.

For residential landlords, stable employment is the foundation of rent collection and renewal strength. If wage growth continues to ease while hiring remains positive, the best outcome for property owners is possible: resilient tenant demand alongside less pressure on central banks to tighten policy further.

The risk is the opposite. If average hourly earnings reaccelerate, bond markets may price in stickier inflation. That would keep mortgage rates and commercial lending costs elevated. In practical terms, higher debt costs compress leveraged returns, lower acquisition capacity, and force buyers to demand wider cap rates.

Manufacturing is another signal worth watching. The ISM manufacturing PMI stood at 54.0 in May, its fourth consecutive month in expansion. That matters for industrial real estate, logistics space, and secondary markets tied to production, warehousing, and regional supply chains. A durable manufacturing recovery can lift demand for light industrial assets, last-mile distribution, and workforce housing near employment nodes.

Oil also deserves attention. WTI crude closed at $69.23, down 9% on the week, despite continuing geopolitical tension around the Strait of Hormuz. Lower energy prices can ease headline inflation and operating costs, particularly for transport-heavy occupiers and landlords facing utility-sensitive expenses. But the geopolitical backdrop remains a risk premium that can return quickly.

The best property strategy this week is not prediction. It is preparation for what rates, wages, and confidence say next.

The technology story is also crossing into real estate. Apple and Microsoft raised consumer product prices, citing memory and storage chip costs driven by AI data-centre demand. That is a reminder that the AI buildout is not only an equity-market theme. It is a land, power, infrastructure, and zoning theme. Data centres continue to reshape demand in select markets, especially where grid capacity and permitting allow scale.

Consumer confidence will help confirm whether households feel secure enough to move, rent, buy, renovate, or trade up. Confidence does not replace income, but it influences timing. In housing, timing matters. A cautious household delays decisions. A secure household signs leases, absorbs inventory, and supports price stability.

For investors, the takeaway is clear. Do not read this week’s data in isolation. Read it as a financing map. Strong jobs support occupancy. Cooling wages support rate relief. Expanding manufacturing supports industrial and regional demand. Lower energy helps margins. The opportunity lies in assets where income durability can withstand today’s cost of capital and benefit when financing conditions eventually loosen.

Source: Yardeni QuickTakes

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")