The Mortgage Lock-In Trade Is Not Over

The most important force in the U.S. housing market may still be the loan homeowners refuse to give up. For investors, that matters more than sentiment. A cheap fixed mortgage is not just a monthly payment advantage. It is a financial asset attached to the house.

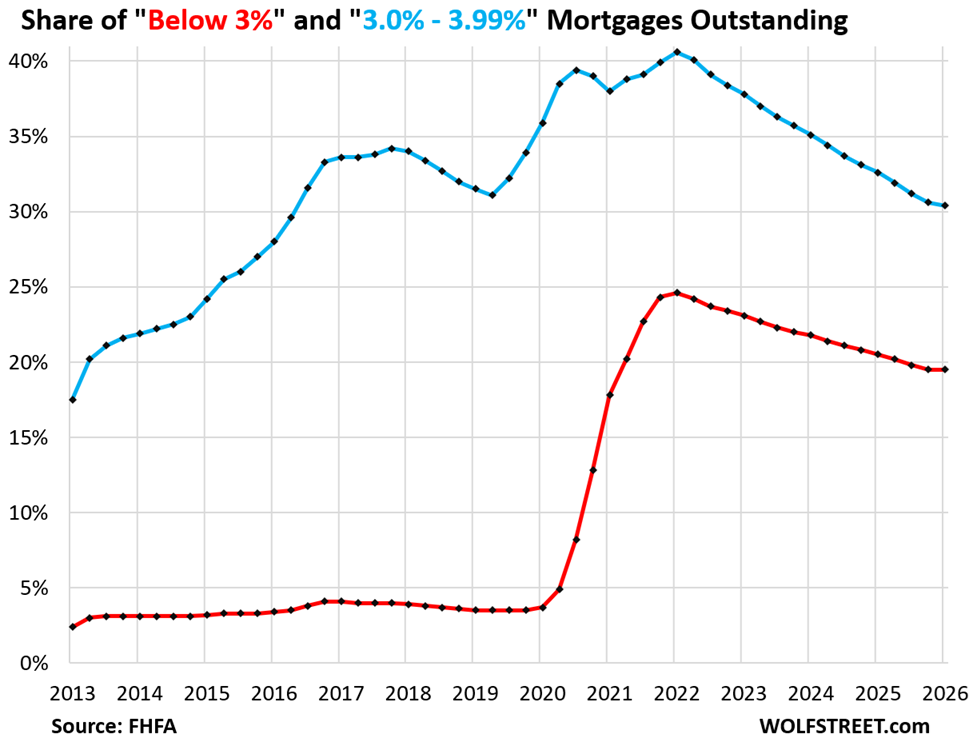

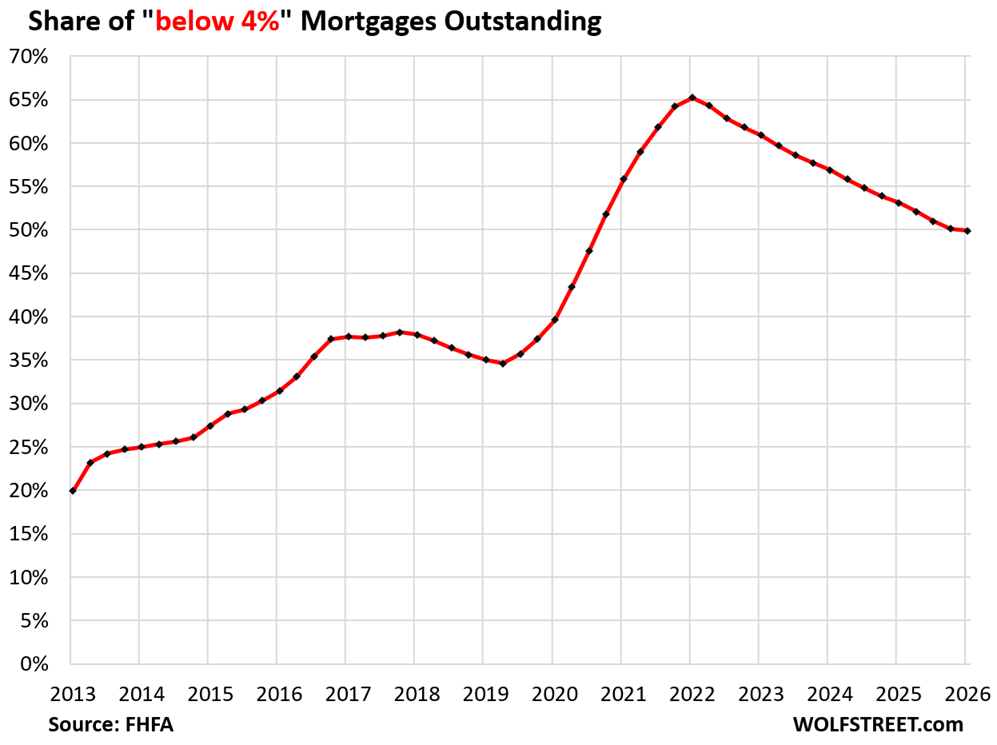

According to FHFA data reviewed by WOLF STREET, the unwinding of the mortgage lock-in effect stalled in the first quarter. Mortgages below 3% remained at 19.5% of all outstanding mortgages, while loans between 3% and 3.99% slipped only marginally to 30.4%. Combined, mortgages below 4% still represented 49.9% of the market.

This is the investment signal: supply relief may be slower than expected. Many forecasts assume that time, life events, and accumulated equity will gradually pull owners back into the transaction market. That process had been underway since 2022. In Q1, it weakened sharply.

For buyers, this keeps the resale market constrained. For landlords, it supports rental demand from households that would normally trade up into ownership but remain priced out by both home values and mortgage costs. For developers, it preserves an opening in markets where new construction is one of the few sources of available inventory.

The lock-in effect is not simply psychological. A homeowner with a sub-3% mortgage is holding debt that is below current inflation and far below prevailing 30-year mortgage rates. Selling that home can mean replacing a highly favorable capital structure with one that materially reduces purchasing power. Rational households do not surrender that advantage unless they must.

A low-rate mortgage is no longer just financing. In this market, it is part of the owner’s balance sheet.

That has direct pricing implications. Limited resale inventory can cushion nominal prices even when affordability is poor. It also means that headline demand weakness may not translate quickly into broad price declines, especially in job-rich metros with limited land, strong household formation, or persistent rental pressure.

But investors should not confuse supply scarcity with risk-free appreciation. A frozen market reduces liquidity. Transaction volume matters to brokers, lenders, flippers, and short-cycle operators. If fewer owners list, fewer comparable sales are created, price discovery becomes thinner, and underwriting becomes more dependent on rent fundamentals and replacement cost.

The other side of the ledger is also shifting. Mortgages at 5% or higher now account for 33.3% of outstanding loans, the largest share since 2016. Recent buyers are carrying more expensive debt, and their flexibility is lower. If income growth slows, taxes rise, insurance costs escalate, or rents soften in overbuilt markets, stress will show first among these newer borrowers, not among owners sitting on ultra-low fixed rates.

Adjustable-rate mortgages remain only 4% of outstanding mortgages, which limits the probability of a broad payment-shock cycle. That is important. This is not a 2008-style credit reset story. It is a structural inventory story, shaped by the legacy of extraordinary monetary policy.

For investors, the practical takeaway is to underwrite local supply with more discipline. Markets with locked-in owners, low new-home production, and durable rental demand may continue to reward patient capital. Markets with heavy new supply, weak income growth, or investor-heavy ownership need more caution.

The best opportunities will not come from assuming rates fall or sellers capitulate. They will come from identifying where constrained resale supply, realistic rents, and long-term demand still align. In a locked market, patience is not passive. It is a strategy.

Source: WOLF STREET

Board Refresh and Index Exit Reframing Its AI Property-Management Narrative?")